News Listing

November 2008

Eleventh

International Symposium on Superalloys

Seven

September 14-18, 2008

Conference

Report Overview

The Eleventh International

Symposium on Superalloys was held at the Seven

Springs Mountain Resort from September 14th-18th. The

conference has been held every four years at Seven Springs since 1968. This

year set a record for attendance with over 461 registrants from countries

around the world. I have attached the list of attendees for reference in

Appendix I. There were ~ 110 papers presented at the conference and published

in the proceedings on CD (PDF files) and in a book of 1000 + pages.

The conference was

organized into six main topical sessions, 1) Alloy Development, 2) Advances in

Processing, 3) Micro-deformation and Macroscopic Properties, 4) Coatings and

Environmental Effects, 5) High Temperature Behavior and 6) Modeling, Simulation

and Validation. The conference organizing committee selected 45 papers for 25

minute oral presentations. The remaining papers were available for discussion

during interactive poster sessions and are included in the proceedings as full

technical papers.

The Conference Organizers and their

affiliations are:

Conference General Chair

Secretary Treasurer Program Chair

Ken Green of RR-Indy;

Jacqui Wahl – Cannon-Muskegon (PCC) Gern Maurer

– Carpenter Technology Roger Reed –

The Eleventh International

Symposium for Superalloys was dedicated to Dr.

Raymond F. Decker, for his substantial and pioneering contributions to the Superalloys field. Ray’s career spans over 58 years

and was highlighted by his technology leadership at INCO (Corporate Vice

President of R&D), Michigan Tech, the Univ of

Michigan and as a co founder of Thixomat. He is noted

for his fundamental work on trace element effects and strengthening mechanisms

in superalloys. His more recent activities at Thixomat have led to the discovery of nanostructured

Mg sheet alloys for autos, aerospace, military armor, batteries, fuel cells and

biomedical implants.

I picked up a great deal of

information from discussions with colleagues, poster session interactions and

in the technical presentations. In the section following my general

observations, I will summarize some of the papers and presentations I thought

were among the most significant. I’ve focused on GT hot section airfoil

material and coating developments and will not address the topic of disk

alloys. I have tried to highlight significant points from these papers and have

included the paper abstract and in some cases figures from the paper as well. I

have organized the papers and my comments by the lead author’s

affiliation. The general observations are compiled from a variety of sources

and serve to provide additional background or context …

General Observations

Rhenium, Ruthenium &

Platinum Market Price Volatility

The topic of Re and Ru market pricing volatility and in some cases inability to

maintain adequate supply to produce alloys (Re) generated substantial

speculation at the conference about the direction the industry would be taking

over the next four years. This year the papers discussing next generation

alloys focused primarily on increased levels of Re and Ru

emblematic of the 4th & 5th generation SX alloys.

Juxtaposed with this trend was GE’s keynote address – they are the

first OEM to publicly announce new low Re or no Re alloys for their (flight)

engines. Purportedly all of the OEM’s are actively assessing their

options for alternative alloy approaches, generating a substantial amount of

alloy development activity behind the scenes. Additionally Rhenium and

Ruthenium are being utilized to increase the temperature capability of current

and next generation MCrAlY overlay coatings used as

TBC bond coats and stand alone environmental protection coatings. Siemens in

particular is committed to Re coating systems. They claimed a 40 – 60 C

benefit with their SiCoat 2464 (Ni-17CR-10Al-1.5Re-0.3Y)

in their paper (Subramanian IGTI paper GT2008-51532). Ruthenium levels up to 1

w/o are disclosed as a further improvement (see US6924046:

“Rhenium-containing protective layer for protecting a component against

corrosion and oxidation at high temperatures” assigned to Siemens)…

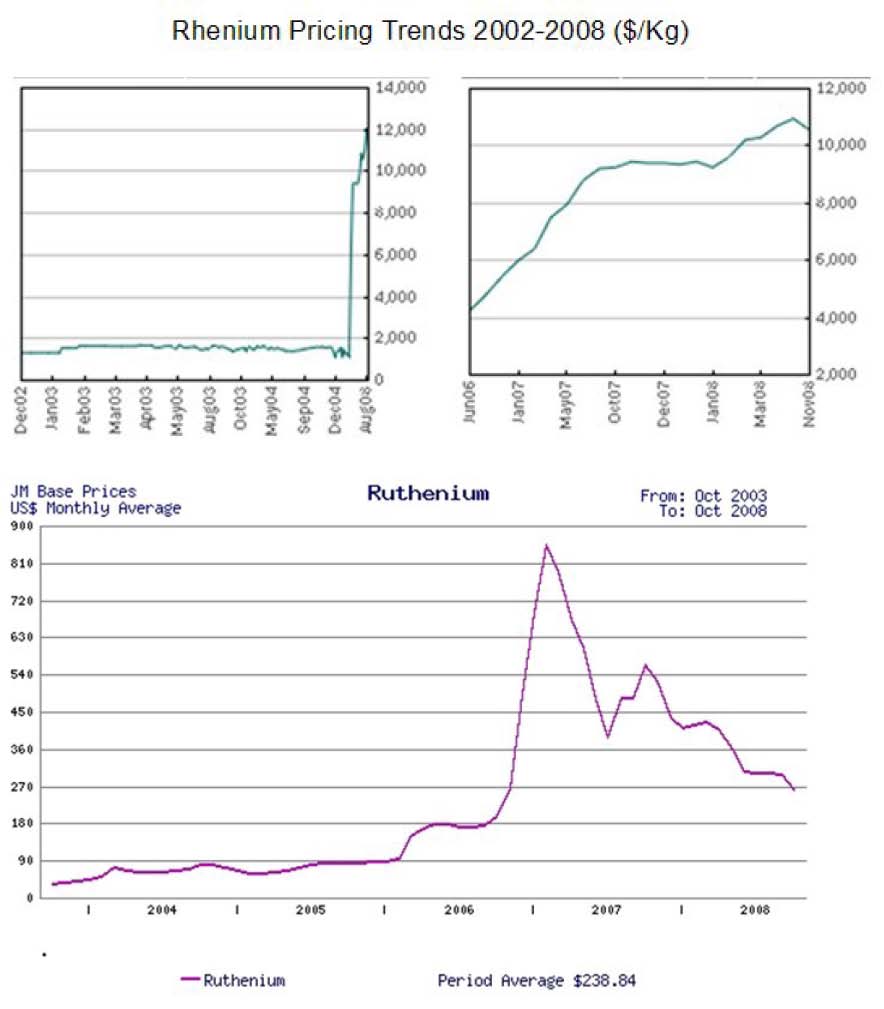

To provide some context for

these concerns, the charts below show the pricing trends for Re and Ru for the last 5 to years. Note that Re is shown in $/Kg

and Ru and Pt are priced in $/Toz

($11,000 / Kg equates to $340 / Toz).

Rhenium pricing has not

fallen recently, unlike Ru or Pt. Since it

isn’t tied to the automotive industry it has remained unaffected by the

current economic downturn. A few quotes help put this in perspective:

“The airline industry's fight for survival in the face of

soaring oil prices has triggered a massive jump in the price of a number of

obscure and scarce metals that are used to improve the fuel economy of jet

engines. Traders said demand for minor metals such as rhenium, chromium, cobalt

and titanium was booming as Rolls-Royce, General Electric and Pratt &

Whitney bought them for new super-alloys that helped cut aircraft fuel

consumption.”

“The jump in the price of rhenium - an extremely rare

metal that was the last naturally occurring chemical element to be discovered -

is the most striking example of the new environment. The rhenium price

yesterday surged to a record of $11,250 a kilogramme,

more than double last year's level and up from about $1,000 in early 2006,

traders said. "At current prices it is more a semiprecious metal than an

industry metal," one trader commented. At current rates, rhenium is only a

little less than half the price of gold - a boon to

By

Javier Blas in London

“Whichever way you look at it, this is still a metal with

not more than 45 mt of new supply each year

(excluding scrap & revert) and demand in the order of 65 mt. Credit crunch or not, any fall in prices can only

therefore be pounced upon by long term buyers grateful for the chance to build

inventory for known future demands. And those demands are building up rather

nicely, $390 bln worth of new aeroplanes

for China by 2027 according to Boeing, or as much as 15 mt

of Rhenium needed for every new GTL (gas to liquid hydrocarbon catalysts

– scrubbing S & Hg) plant, or just simply an average of

about 25 kgs for every new jet engine. One mind-blowing

calculation is that if you take Boeing`s estimate of

almost 30 000 new aeroplanes by 2027 and multiply by

a low of 20 kgs Re per engine, the aeroindustry needs on average 60 mt

of Rhenium a year for next two decades.”

“With the top three consumers GE, Pratt

& Whitney and Cannon

Rhenium

Defies Downturn 2008-03-08 Lipmann Walton & Co

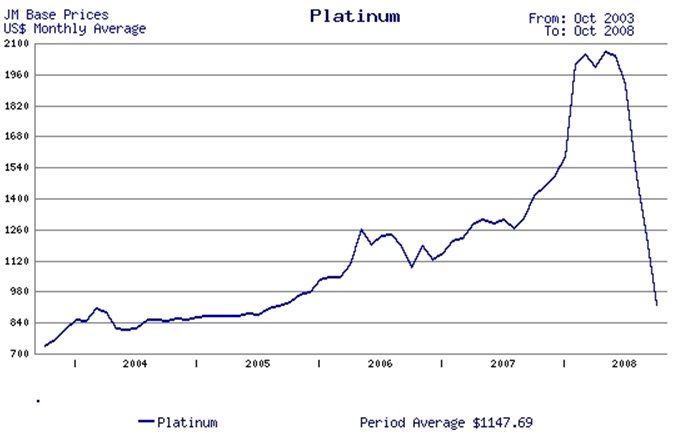

Platinum has also shown

pricing volatility as illustrated in the five year monthly average pricing

chart from Johnson-Matthey. Platinum is used for TBC bond coatings on aero

engines for GE, RR & Honeywell among others. Platinum is also used extensively

in the superalloy casting process to help position

ceramic cores relative to the ceramic shell, maintaining airfoil wall. GE

announced their next generation NiAlCrZr bond coating

(flight engines) at the conference. In addition to improved TBC life, lower

cost was also considered to be a strong driver when Pt hit its peak of $2276 in

March. With the dramatic fall in auto sales and overall economic downturn the

Pt price is likely to remain in the trading range $700-900 / Toz or lower.

Please contact me regarding

additional information or for a copy of the complete report (34 pages)

summarizing my observations and commentary from the Superalloys

2008 Conference.

Material Processing Technology, LLC

Phone 231-780-1265; e-mail JeffSmith@mpt-llc.com

Copyright 2008